Home | Personal Advice | Personal Columnists | Situation Analysis

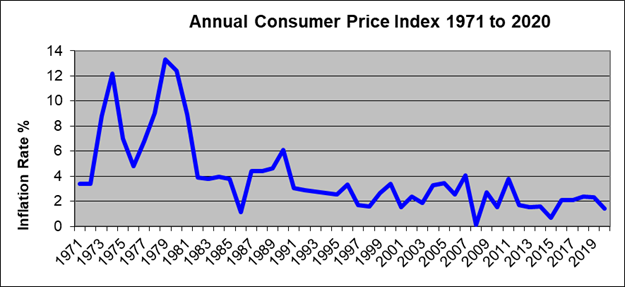

Since the 1980’s few people have experienced high inflation. Because of this many people do not know what it is and how it can affect us. Here is a brief introduction to inflation. What is Inflation?Aside from baby boomers and their parents, few people have suffered through a sustained, high inflation environment such as we experienced in the late 1970s and early 80s. For the last 40 years, inflation, as measured by the Consumer Price Index (CPI), has been on a mostly uninterrupted descent, and it has not been much of a factor at all over the last ten years.

That all changed abruptly in April 2021 when the inflation rate spiked, recording the most significant year-over-year increase in several decades. Suddenly, with the media, politicians, and economists sounding alarms over “the return of inflation,” people are interested in this “new” economic phenomenon. What is important to know is how inflation impacts our financial futures as well as our daily lives. A Simplified Explanation of Inflation For as long as people have exchanged goods for money or other goods, inflation has lurked among us. We learned through our high school textbooks that inflation is the result of too many dollars chasing too few goods. When the economy is growing, higher consumer spending has the effect of pushing up demand. When demand (with more dollars behind it) exceeds the available supply of goods, it drives up prices. A more recent history of inflation shows that it is increasingly driven by the supply of money, which is controlled by monetary policies. When the economy turns sluggish, as evidenced by higher unemployment, the Federal Reserve can step in and start “printing money” to stimulate the economy. The Fed creates money by buying U.S. Treasury bonds, such as during the economic crash in 2008 and more recently during the COVID crisis. It can also lower short-term rates to encourage bank lending as another way to stimulate economic growth. Both policies can lead to “too many dollars chasing too few goods” if the economy grows too fast. How Inflation is Measured At its core, inflation is a measure of the rate of change over time in the average price level of selected goods and services. The CPI is the standard measure of inflation. The index consists of a basket of commonly purchased goods, such as food, transportation, medical care, entertainment, among many others. Each month, the U.S. Bureau of Labor Statistics tracks the prices of hundreds of goods to come up with a current CPI rate. When the rate is published each month, it represents the year-over-year change from the same month in the prior year. For example, the 4.2% increase in April 2021 is how much it changed from April 2020. The significant spike can be attributed to the fact that in April 2020, the inflation rate was virtually zero due to the COVID-induced economic downturn. So, even a minuscule increase in the April 2021 inflation rate would produce a large spike. By July 2020, the inflation rate resumed its normal trajectory so, the changes in CPI should be more moderate. The annual CPI rate, which was just 1.4%, is the average rate of change over the course of the year. Why it’s Important to Track Inflation The inflation rate can impact our lives in many ways—in our cost of living, how much we pay in interest, and our ability to retire comfortably. Understanding inflation trends is critical to planning for current spending as well as future income. Inflation can also impact the performance of your investments. Loss of Current Purchasing Power When the price of goods increase, you need to increase your spending, which can affect your lifestyle in several ways. When grocery prices rise, you either have to budget more for food items or lower the quantity or quality of the goods you usually purchase. When gas prices rise, you either spend more or drive less. Either way, rising prices make it more challenging to save for your future. Pay More in Interest One of the primary tools the Fed uses to combat inflation is to increase interest rates. The increase in short-term rates can have a ripple effect on all forms of debt, including mortgages, credit cards, auto loans, etc. Poor Investment Performance Inflation can also erode your investments. When interest rates rise, it can lead to lower bond values and weaker stock prices. When inflation expectations increase, consumers brace for higher prices on goods and services now, putting less weight on their investment assets, leading to lower asset prices. Positive Effects of Inflation Moderate inflation can also have a positive effect on the economy. When price levels increase gradually, consumers are more likely to make purchases now to avoid paying higher prices in the future. This can have a stimulative effect on the economy, increasing demand. In the short term, this can increase retail sales and the production of goods. Companies will need to hire more workers, which can boost economic growth. Mild inflation also reduces the risk of deflation, which can be even more harmful to the economy than inflation. When prices fall due to an economic downturn, consumers will wait to make purchases if they believe prices will fall further. The reduced demand results in businesses cutting back on inventory and production, increasing unemployment and wage deflation. Consumer spending will decline even further, exacerbating declining demand and price reductions, which could force some businesses to close. A deflationary cycle can be devastating and challenging to end. That’s why allowing for mild inflation growth can be healthy for the economy. |

|

Read other situation analysis articles |

|

|